The proliferation of options strategies in recent years reflects the growing investor appetite for options. For those investors just getting started in options, long calls and long puts create the foundation for many options strategies.

Long Calls

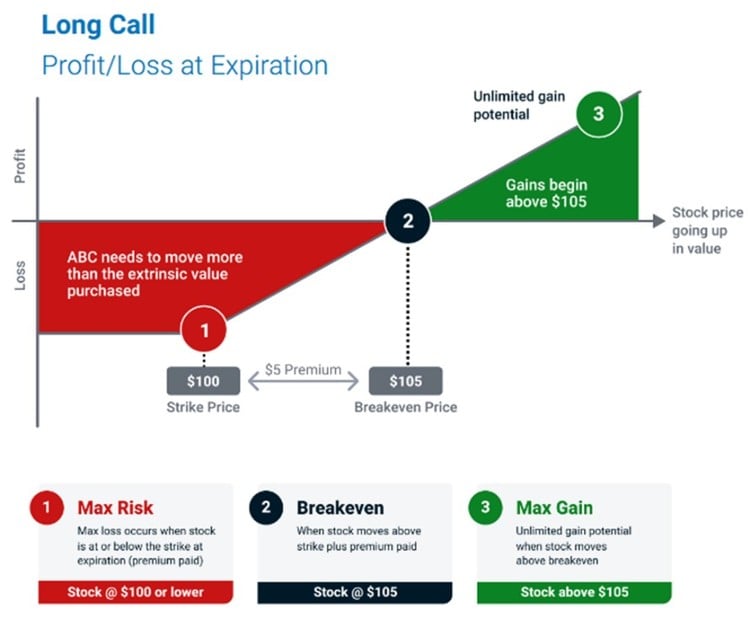

Call options give an investor the right, but not the obligation, to purchase an underlying asset at an agreed-upon price — called the strike price — by an agreed-upon expiration date. The buyer of a call pays a premium for the call option and may exercise it at any point up until it expires. Long calls refer to buyers, while short calls, covered separately, refer to sellers. A buyer’s risk is limited to the cost of the premium, while the return potential is unlimited, BMO explained in an options explainer course.

Long calls are bullish and prove favorable for buyers when markets are rising. By purchasing a long call, an investor makes money when the market price rises above the strike price plus the premium paid. For example, if an investor bought an option of stock XYZ with a strike price of $200 for a premium of $10, the breakeven point would be a market price for the underlying asset of $210.

“On expiration, an option is generally worth only its executable value – this [is] also called in-the-money (ITM) value or intrinsic value,” noted BMO.

Several elements go into determining an option’s premium, but time plays a pivotal role. The longer an option has to expire, the higher the premium. This occurs because an option is more likely to cross the strike price or become in-the-money. Sellers are compensated for this higher risk in the form of higher premiums. Therefore, long calls with longer days to expiration (DTE) cost more than those with a shorter DTE.

Long Puts

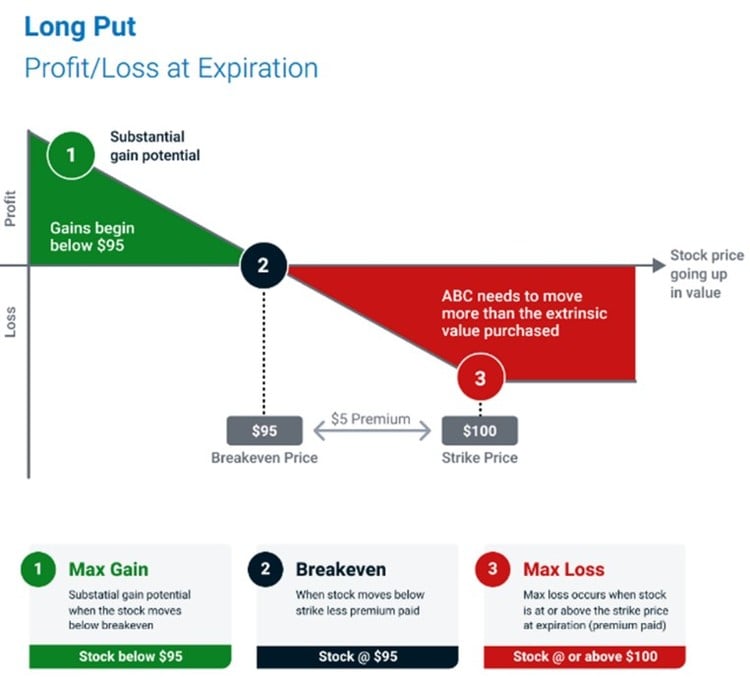

Long puts are the inverse of long calls. They give the buyer the right, but not the obligation, to sell an underlying asset at an agreed-upon strike price by a certain date. As with long calls, a long put refers to the buyer of the option. They’re a bearish strategy because buyers benefit when markets decline. Risk for long put buyers is limited to the cost of the premium with notable return potential should prices decline significantly.

“A long put is bearish and profits from a sharp downwards movement in the underlying,” BMO wrote. “As the underlying position can decrease to zero, the strategy has substantial profit potential.”

As with long calls, long puts are also more expensive when they have longer DTE. “All else equal, time works against this strategy,” explained BMO.

This article is prepared as a general source of information and is not intended to provide legal, investment, accounting or tax advice, and should not be relied upon in that regard. If legal or investment advice or other professional assistance is needed, the services of a competent professional should be obtained. Information contained in this article does not constitute and shall not be deemed to constitute advice, an offer to sell/ purchase or as an invitation or solicitation to do so for any entity. The content of this article is based on sources believed to be reliable, but its accuracy cannot be guaranteed. BMO InvestorLine Inc. and its affiliates, sponsors and employees do not accept responsibility for the content and makes no representation as to the accuracy, completeness or reliability of the content and hereby disclaims any liability with regards to the same. Any strategies discussed, including examples using actual securities, quotes and price data, are strictly for illustrative and educational purposes only and are subject to change without notice. BMO InvestorLine Inc. is not responsible for the information provided and disclaims all liability with regards to the same.

BMO InvestorLine Inc. is a member of BMO Financial Group. “BMO (M-bar Roundel symbol)” is a registered trademark of Bank of Montreal, used under licence. BMO InvestorLine Inc. is a wholly owned subsidiary of Bank of Montreal. Member – Canadian Investor Protection Fund and Member of the Canadian Investment Regulatory Organization.